Nothing Stops This Train

And We’ve Been Riding It for Years

Lyn Alden recently in her Thoughtful Money interview shared her views on US and what is happening around the globe and the precarious situation of the financial system, and the familiarity of the ideas was striking.

At Pinetree Macro, we’ve been drawing the same conclusions, just in expressing the same ideas differently.

We have tried to present the overlap of our views in an attempt to explain what lies in store for Investors

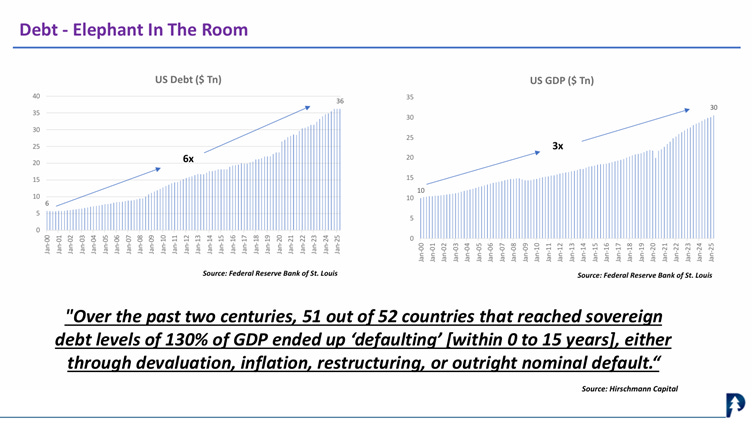

1. The Debt Is the Story.

US debt has gone 6x in 25 years. GDP has gone 3x. That gap is the entire argument.

Over the past two centuries, 51 out of 52 countries that hit 130% debt-to-GDP defaulted within 15 years, through devaluation, inflation, or restructuring. The US crossed that level in 2022.

Lyn’s view: The deficit won’t be cut. The train keeps rolling. No hyperinflation, no sudden collapse, just a long grind of fiscal dominance where the government crowds out everything else.

Our view: The only question worth asking is not if they default, but what form the default takes. Once you answer that, the portfolio writes itself.

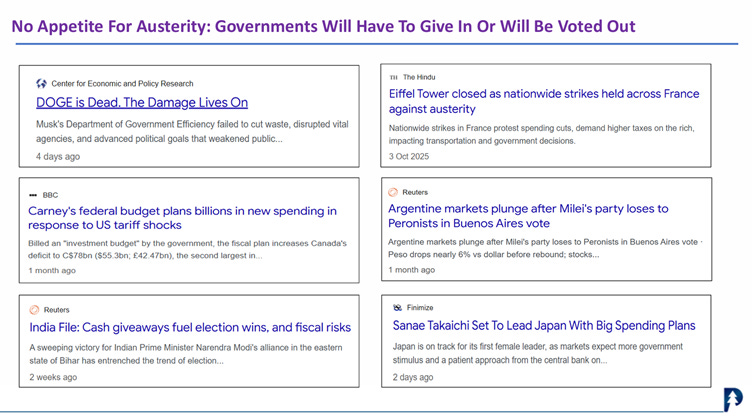

2. Austerity Is Dead. Governments Know It.

Lyn’s view: The gray zone persists because cutting spending is politically impossible. Politicians who try get voted out.

Our view: We’ve been making this point for two years. DOGE failed. France had nationwide strikes. Canada is expanding its deficit. India wins elections with cash giveaways. This isn’t a forecast anymore; it’s the news cycle.

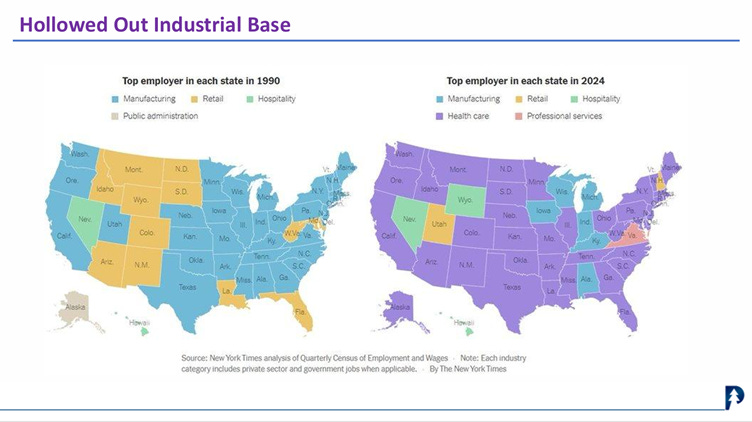

3. The Hollowed-Out Economy Explains Everything

In 1990, manufacturing was the top employer in most US states. Today it’s healthcare administration in 39 out of 51 states.

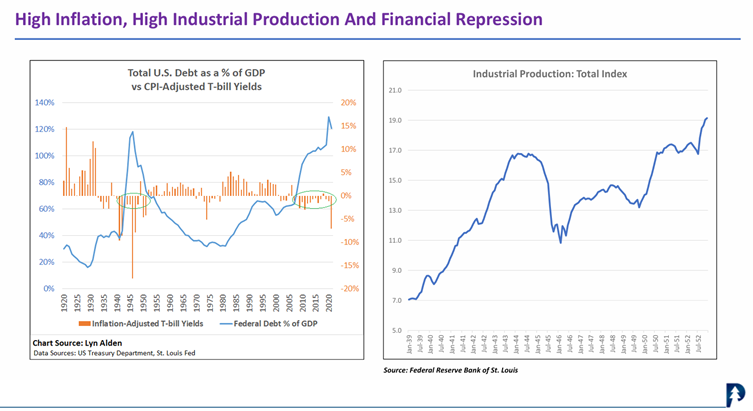

The consequence: A country that builds nothing cannot service a $38 trillion debt through real growth. So, it inflates instead. Financial repression, keeping rates below inflation for years, is the post-WWII playbook, and it’s being run again.

The chart says it all. Last time the US had debt at 130% of GDP, they used exactly this tool. Bond holders lost real wealth for a decade. Real asset owners did not.

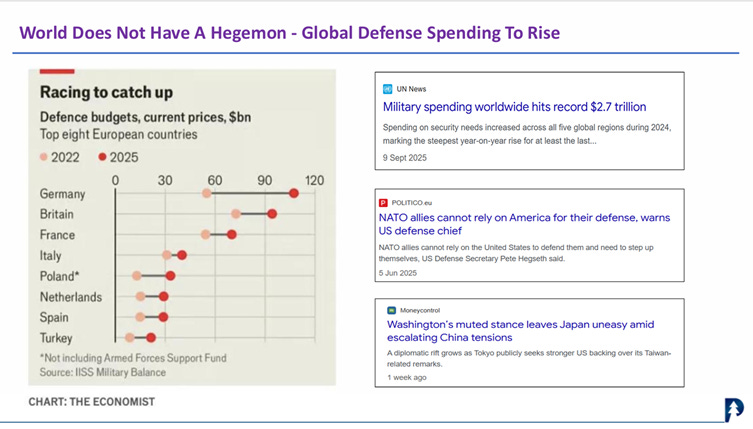

4. The Hegemon Has Left the Building

Military spending just hit a record $2.7 trillion globally. NATO allies are racing to rearm. The US Defence Secretary told allies they can no longer rely on America for their defence.

Lyn’s view: The US is elegantly right sizing its global role. A gradual, managed retreat as the dollar’s reserve status slowly shrinks.

Our View: Empires don’t pick fights with their own allies. The US is threatening Canada, imposing tariffs on Japan, and abandoning NATO partners it has protected for 50 years. US is retreating.

The EU promised $600 billion in US investment and couldn’t back the promise within 24 hours. Japan and South Korea are being squeezed simultaneously. This is not a managed retreat; this is a regime change in American foreign policy.

We had written six months before Trump was inaugurated President, a Trump presidency would accelerate deglobalisation, push every country to fund its own defence, and lead to a multi-currency trading system. It was a pure macro call. It would have been the same under Harris.

The investment consequence is urgent, not gradual: global defence is a decade-long structural Supercycle. Every country that relied on the American umbrella is now writing cheques. European, Japanese, Korean, and Indian defence are decade-long compounders.

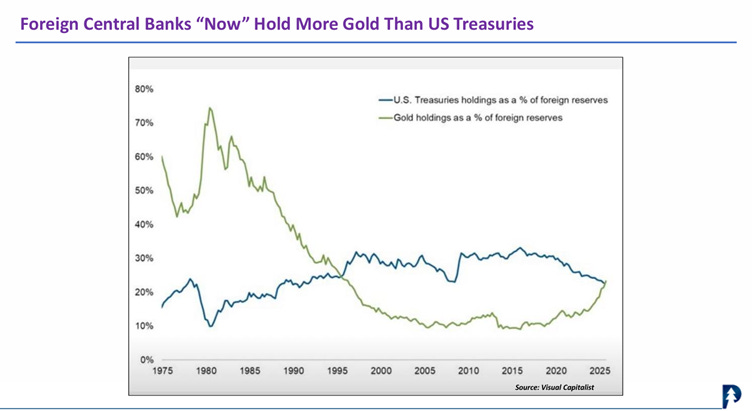

5. The Dollar Is Already Breaking Down

The USD trade-weighted index has broken its multi-year uptrend. This isn’t prediction, it’s already on the chart.

Lyn’s view: The dollar’s exorbitant privilege is fading. To rebalance trade, the US needs a weaker dollar and must accept a smaller share of the global reserve system.

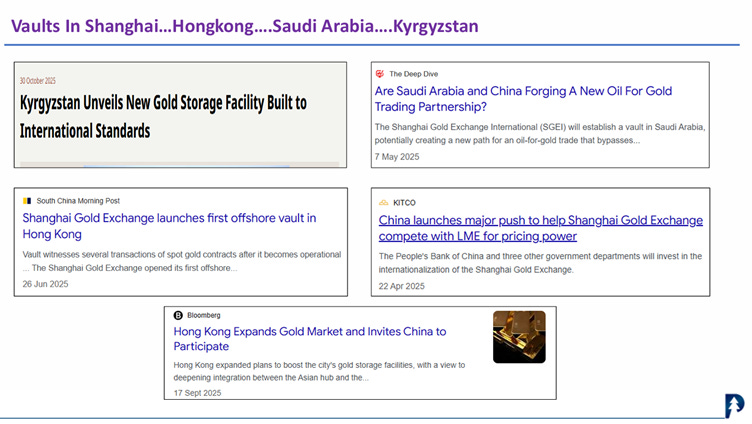

Our view: The evidence is already in. Central banks now hold more gold than US Treasuries, for the first time since 1992. Vaults are opening in Shanghai, Hong Kong, Saudi Arabia, and Kyrgyzstan.

That crossover chart is the single most important investment signal of this decade. When central banks swap Treasuries for gold, they are voting with real money on where the monetary system is heading.

This is not speculation. It is infrastructure being built for a post-dollar settlement system.

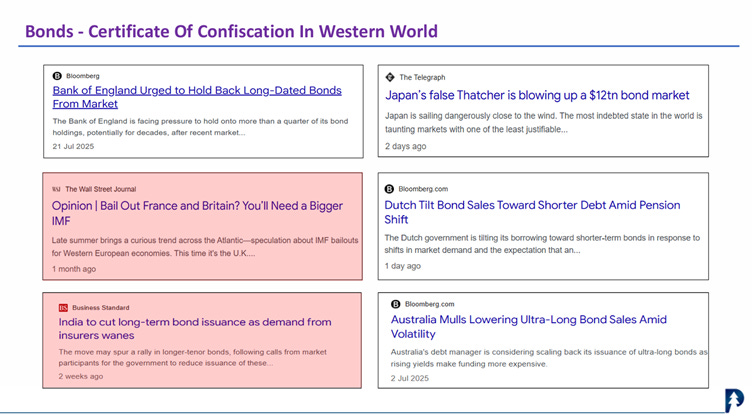

6. Bonds Are Certificates of Confiscation

The Bank of England is being asked to hold bonds for decades. Japan’s bond market is under stress. Australia is cutting ultra-long issuance. Western governments are quietly admitting that bonds at current yields cannot hold.

Both our views merge: in a world of fiscal dominance and debasement, holding long-duration bonds in Western currencies is a wealth destruction strategy. The real yield is negative when you do the honest accounting.

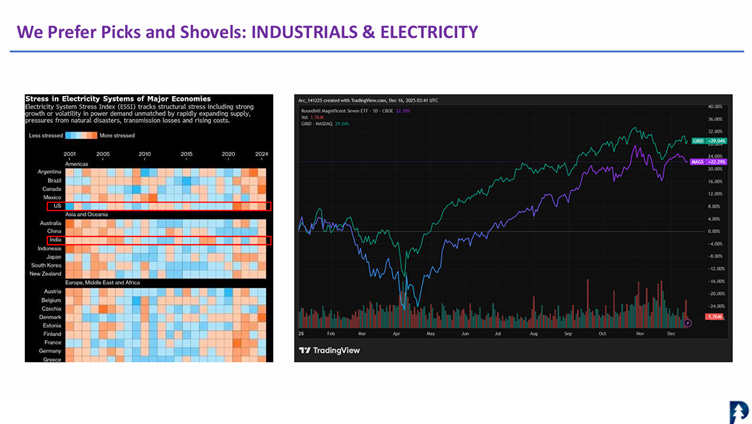

7. AI Is Real - But the Grid Is the Actual Investment

The GRID ETF has outperformed the Magnificent Seven by a wide margin over the past year. The chart is not subtle.

Lyn’s view: AI is a genuine white-collar productivity revolution. But energy is the single biggest binding constraint. The human brain runs on 20 watts. AI data centres do not.

Our view: Electrification has been our macro theme of the decade. AI has just accelerated it. We don’t care which AI model wins, every single one needs copper, uranium, and a functioning grid. Picks and shovels, not the gold rush.

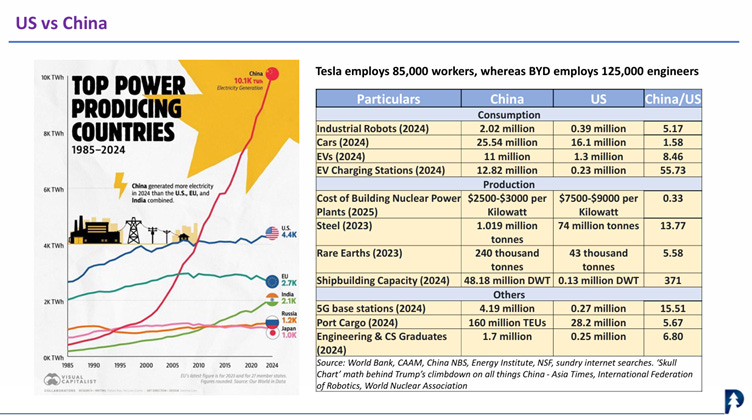

China generates more electricity than the US, EU, and India combined. It builds nuclear plants at one-third the US cost. It has 371x the shipbuilding capacity. The idea that the US can re-industrialise quickly without a decade-long infrastructure build is a fantasy.

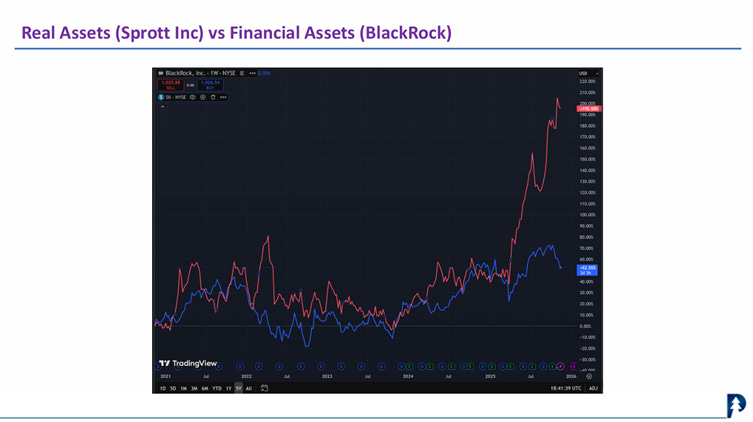

8. The Rotation Has Already Begun

Sprott, the real assets manager is up nearly 200% over five years. BlackRock, the financial assets manager is up roughly 50%. The market is already telling you where capital is going.

Lyn’s view: Hyperscalers are transferring value from their shareholders directly into the physical economy through capex. The winners are commodity producers, energy infrastructure, and value stocks with real cash flows.

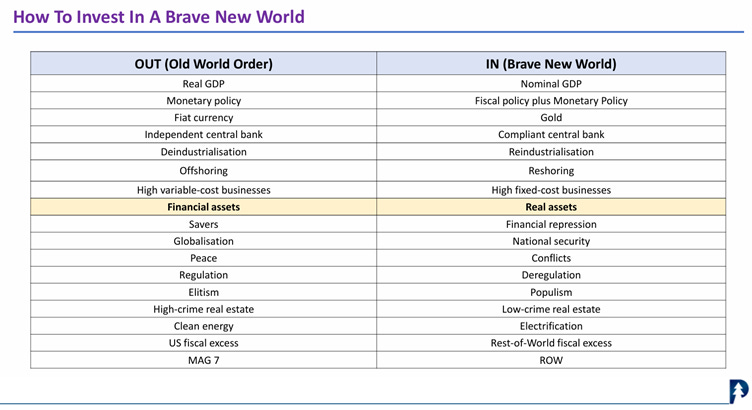

Our view: This is the Brave New World a rotation we have been positioned for. The table below from our December 2025 CFA presentation says it plainly:

The Bottom Line

Lyn Alden maps a multi-decade gray zone of fiscal dominance, gradual debasement, and capital rotation into real assets. That is exactly the Brave New World we have been positioning for since 2022.

Russell Napier validated this thesis through financial history. Lyn Alden has now validated it through monetary mechanics.

The wealth transfer from paper assets to real assets is not coming. It is already underway. The only question is which side of it you are on.

The train has left the station. Pack accordingly.

Lyn Alden’s views are drawn from her February 2026 interview on Thoughtful Money with Adam Taggart. Her research is at lynalden.com. Slides are from the Pinetree Macro Global Macro Outlook 2026 presented at CFA Society Bombay, December 2025.

This article reflects the views of Ritesh Jain and Pinetree Macro. Not financial advice.

Curious how you think about timing within this broader shift, especially for someone who cannot constantly rebalance. How do you think policymakers might respond if inflation stays persistent but growth weakens at the same time, especially when both monetary and fiscal tools are already stretched?